Composites industry heads into slightly accelerated contraction in November

The GBI: Composites Fabricating in November continued its general slow-going path of contraction that began in April 2023.

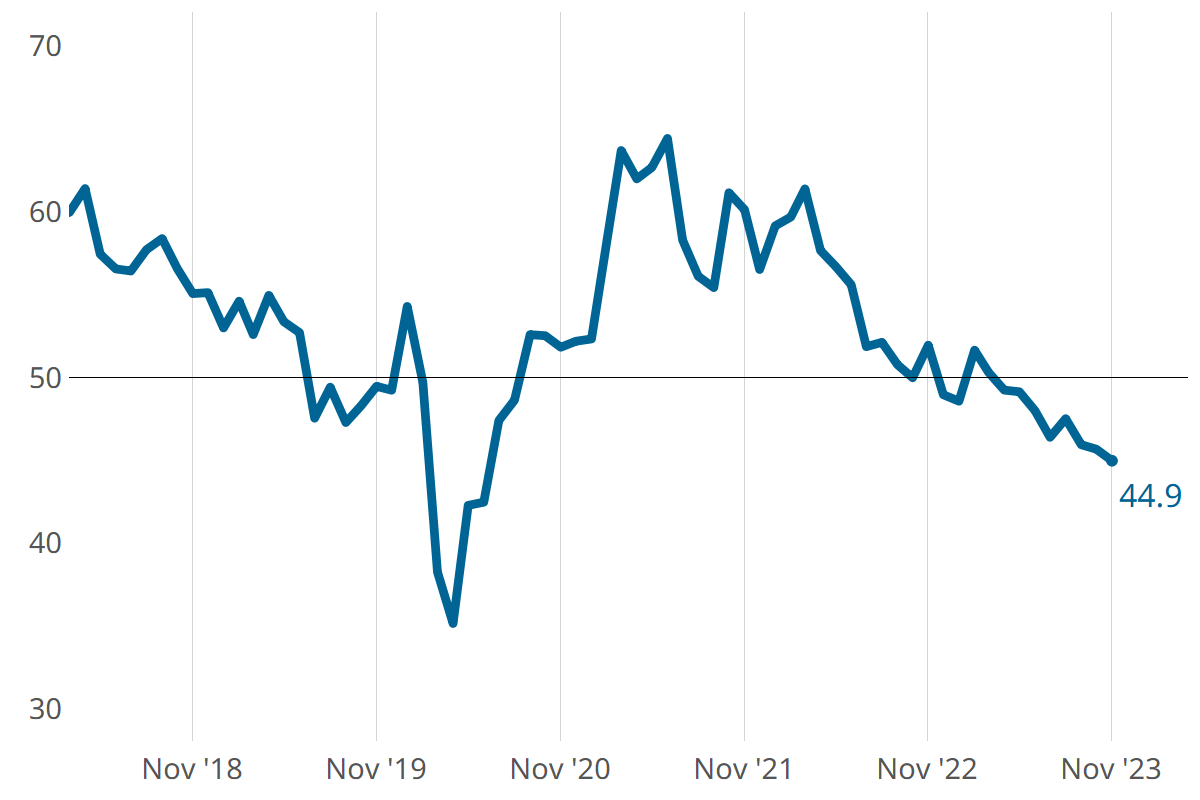

Taking a step back. GBI: Composites Fabricating in November was down 0.7 points relative to October. Photo Credit, all images: Gardner Intelligence

The GBI: Composites limped along again in November, experiencing minorly accelerating contraction to about the same degree as October, closing at a reading of 44.9 compared to the previous month’s 45.6. This general slow-going contraction began in April 2023.

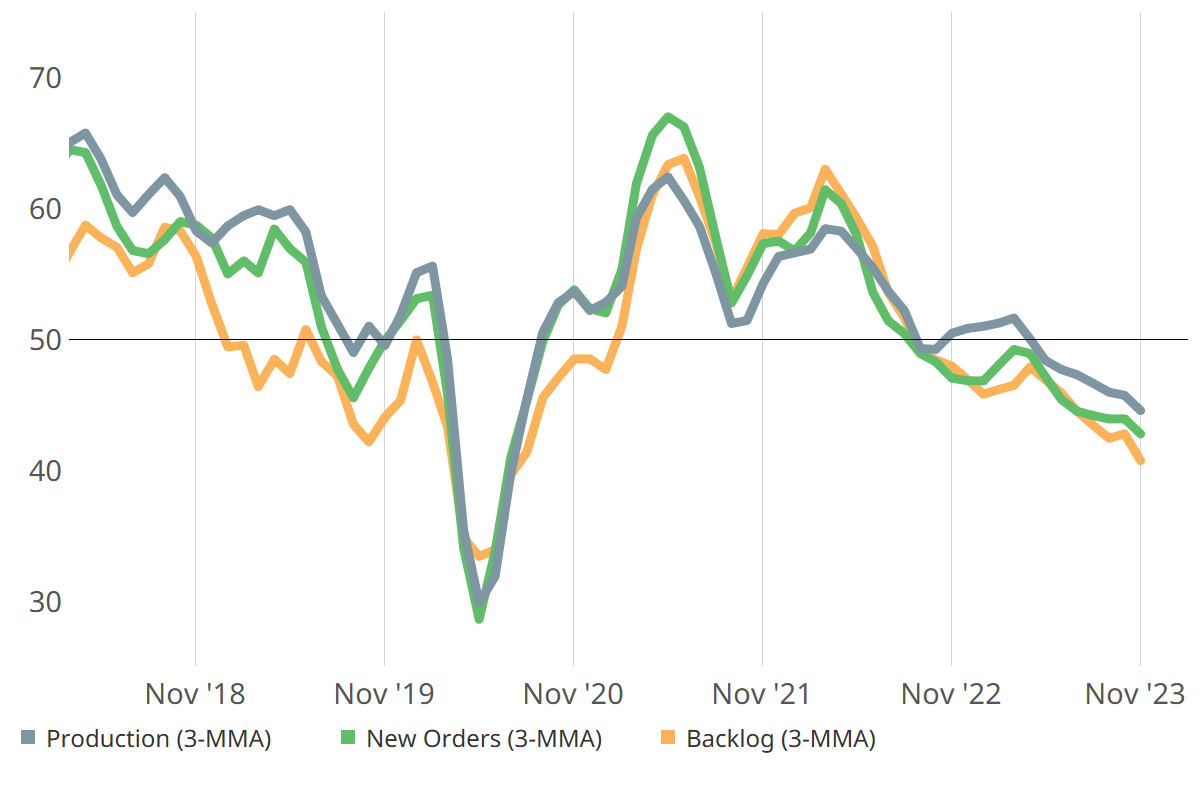

Closely connected composites fabricating components — production, new orders and backlog — primarily drove November contraction. Exports marched along its slowly accelerating contraction path while employment contraction slowed a bit, potentially starting a return to a more normative state following the accelerated contraction that emerged in August. Supplier deliveries continued to lengthen, but at a slowing rate that inches it closer to flat every month.

Downward spiral. Production, new orders and backlog components drove November’s accelerated contraction. (This graph is on a three-month moving average.)

Related Content

-

Index remains in expansion territory despite uncertainties

The composites market saw a slight decline in the index, component and future business results but maintained a positive reading overall.

-

Composites market continued expansion activity into February

GBI: Composites Fabricating’s final reading landed at 52, driven by strong component readings across the board.

-

Contraction slows for second month, with some indicators improving

In September new orders and employment were up slightly, future business outlook improved and material prices dropped.